Throughout my time being active in politics, people have discussed the rise of Neo-Liberalism and the free market that occurred throughout much of the world from the late 1970s onwards. Yet few seem to really understand the reasons for this significant shift in economic policy at that time, which continues to shape our society today.

Those less familiar with the works of Karl Marx may not be familiar with the concept of the tendency for the rate of profit to fall. One does not need to be a Marxist nor socialistically inclined to believe or understand this law of economics, which explains what has happened in the last half-century of economics. As Wikipedia explains:

The tendency of the rate of profit to fall (TRPF) is a hypothesis in the crisis theory of political economy, according to which the rate of profit—the ratio of the profit to the amount of invested capital—decreases over time. This hypothesis gained additional prominence from its discussion by Karl Marx in Chapter 13 of Capital, Volume III,[1] but economists as diverse as Adam Smith,[2]John Stuart Mill,[3]David Ricardo[4] and Stanley Jevons[5] referred explicitly to the TRPF as an empirical phenomenon that demanded a further theoretical explanation, although they differed on the reasons why the TRPF should necessarily occur.[6]

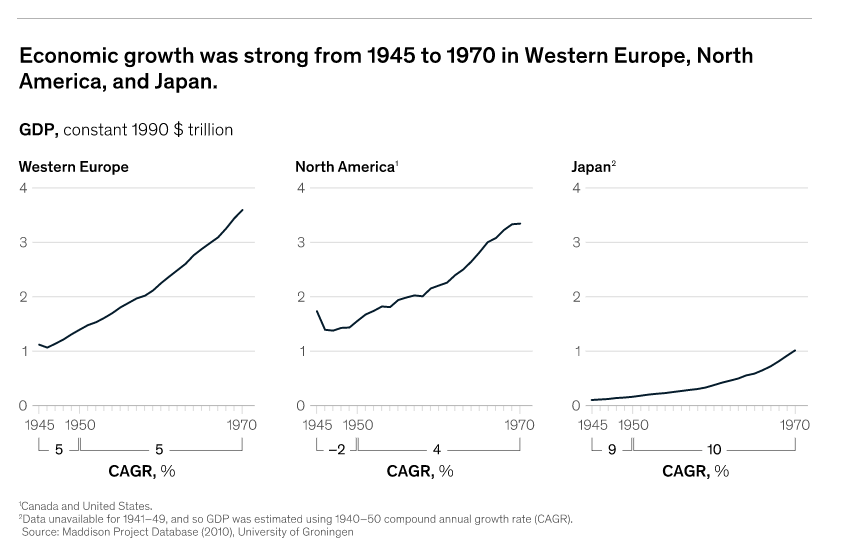

To simplify this concept in explaining what happened in the late twentieth century we simply need to understand that in response to the 1930s depression many nations and particularly developed nations invested in infrastructure to stimulate their economies and create employment. This was followed shortly by the Second World War where investment in industry was required. Then after the war, the Marshall Plan rebuilt Europe, whilst similar investment and rebuilding occurred throughout the late 1940s. This period of investment in response to the depression and war created the post-war boom resulting in significant economic growth.

Keynesian economics whereby government policy and intervention in the economy and significant levels of government spending are required to stimulate the economy and prevent depressions. This theory dominated government policy in economically well-off nations from Great Depression until the mid-1970s, when the post-war boom came to an end. The thing Keynesian economics was meant to prevent happening, did happen. So in 1979, Margaret Thatcher came to power in the UK, and the following year Ronald Reagan in the US, and with them came a sea change in economic policies not just in their own countries but internationally.

The Neo-Liberal project essentially was to move away from state intervention and allow the invisible hand to do its dirty work. Privatisation of state infrastructure such as rail or power companies, reducing spending on public services and increased user pay charges, and generally reducing the size of the state to try and stimulate the private sector. Part of this also included reducing employment rights including laws protecting the right to collectively organise, ultimately resulting in reduced earnings for most people. As my series of blog posts about the trade union movement suggested, the job of those wishing to attack union rights was often made much easier by the fact that most union leaders and a poor understanding of economics or how to respond to the end of the post-war boom.

New Zealand was peculiar in its transition to Neo-Liberalism in that it was the Labour Government of 1984 to 1990 that first introduced and championed these right-wing economic policies. At the time the big political issue in New Zealand was the Nuclear Free movement which successfully stopped US Nuclear ships from visiting New Zealand. Whilst this was a worthy campaign, it is strange to think that a government selling off state assets (often for less than their market price) and putting thousands out of work managed to win support based on a Nuclear shipping policy when their economic decisions were hurting so many.

Neo-Liberalism and reducing the size and expenditure of the state were meant to stimulate the economy. For whatever short-term gains were made in the 1980s and 1990s, which generally only benefited the 1% wealthy elite, it soon became clear that the fundamental problems in the economy still remained. Unregulated or self-regulating markets resulted in terrible outcomes including the Pike River mining disaster in New Zealand, the Grenfell Tower fire in London, and the levee failures in New Orleans during Hurricane Katrina all from lack of regulation and investment by the Government.

The 2008 crash ended the widely held belief that the market could correct itself or that wealth would trickle down. This crisis was due to a lack of financial regulation and was then made much worse by those countries who insisted on implementing austerity measures to restore public finances, instead of making the economic situation worse. Neo-Liberalism now is discredited and few governments either on the left or right really have an appetite for the types of policies Thatcher and Reagan promoted 40 years ago. As I will discuss in another blog post on Liz Truss’s brief time as Prime Minister, attempts to follow such a path now generally end in disaster very quickly.

After the fall of the Eastern Block Communist/Marxism ideology has been largely discredited. The end of the post-war boom saw an end to Keynesian economics and a shift to Neo-Liberalism, which is now also largely discredited. In 2021 economic policy is largely populist and a weird mix of Keynsian/Keynesian-lite interventionism with a sprinkling of laissez-faire rhetoric. So far in the 21st century, Capitalism has lacked any serious rivalry from any other theory or system. But capitalism has also run out of ideas. This is not just an abstract notion as the political upheavals in recent years stem from people feeling let down and angry by an economy that has not delivered. Yet, there is no clear alternative to the status quo. People were shocked in 2016 when the UK voted for Brexit and the US voted for Donald Trump as President. The increasingly polarised and challenging political world we live in can be blamed on many different factors. But at its core, I believe much of the trouble is caused by the lack of economic policy ideas that can address some of the great challenges we face.

We can learn much from mid-20th century Keynesian economics, but we also need to understand the limits of this theory and what caused the shift away from them from the late 1970s. Whilst the Neo-Liberal experiment also failed, we should also understand that bureaucratic and cumbersome regulation must have a purpose, and whilst state investment in public services can have real benefits we must be clear about what these actually are when this money is spent. Whilst I subscribed to socialist ideas in the past, it is clear that attempts to implement such a system to date have all ended in failure. However, we can still take Marx’s economic analysis (if not subscribing fully to his proposed remedy), specifically what he had to say about the tendency of the rate of profit to fall. Before we decide whether the current economic system can be reformed or needs to be completely replaced, we first need to improve the general understanding of how our economic system works.

One thought on “The end of the post war boom”